Is there a case for financial literacy education in high school?

- Oct 28, 2025

- 2 min read

I recently moved to a new high school, and one of the first differences I noticed was the graduation requirements. At my old school, financial literacy wasn’t even offered as a course. At my new school, you need at least 0.5 credit in personal finance to graduate.

This change got me thinking: Why isn’t financial literacy a universal requirement, especially considering how essential financial decision-making is to adult life? The lack of consistent financial education across school systems seems like a missed opportunity. From what I’ve seen, a lot of people my age don’t understand concepts like how compound interest works, how credit card payments are structured, or how unpaid balances can quickly spiral because of interest rates. The current landscape makes me wonder whether a poor understanding of financial concepts impacts more than just individuals—potentially influencing the broader economy as well. Data has shown that many college loan borrowers attend college with no understanding of financial aid and without fully understanding how much debt is appropriate and how to compare it to expected income level upon graduation.

Out of curiosity, I started looking into studies on this topic. Some showed promising results. For example, The Effects of High School Personal Financial Education Policies on Financial Behavior found that students who took financial education were less likely to default on credit card payments and had higher credit scores later on. Another one, State-Mandated Financial Education and the Credit Behavior of Young Adults, had similar findings.

The gold standard of studies: a randomized controlled trial was performed in Spain. The Impact of High School Financial Education on Financial Knowledge and Saving Choices enrolled 3000 9th grade students across the country. The students received a financial education course and scored higher in post course testing. Additionally, they had more patience in saving choices. The effects lasted for 3 months when the students were compared with a control group in an incentivized saving task.

But not all studies agree. One paper, How Does Financial Education in High School Affect the Subjective Financial Well-being of Adults?, used a five-item scale developed by the Consumer Financial Protection Bureau (CFPB) and found that financial education seemed to help more for men than women. I wonder if the results are influenced by income level, job opportunities, or other factors.

And when it comes to long-term impact—like saving for retirement—the evidence is even less clear. A study called Does Financial Education Affect Retirement Savings? found little to no lasting effect.

The Effects of Financial Education on Short-term and Long-term Financial Behaviors estimated how financial education in high school, college, or through an employer affected a person’s short- and long-term financial behaviors. They used data from the 2012 National Financial Capability Study (NFCS). They found mixed effects on behaviors that have short term feedback. Financial education has positive effects on long-term behaviors which do not have immediate feedback- that is promising!

So, is financial literacy education worth it? From what I’ve read and seen, it definitely helps with short-term money management and builds confidence. But whether it changes long-term financial behavior, especially across different income levels, is still up for debate. Intuitively, I consider it to be an important skill.

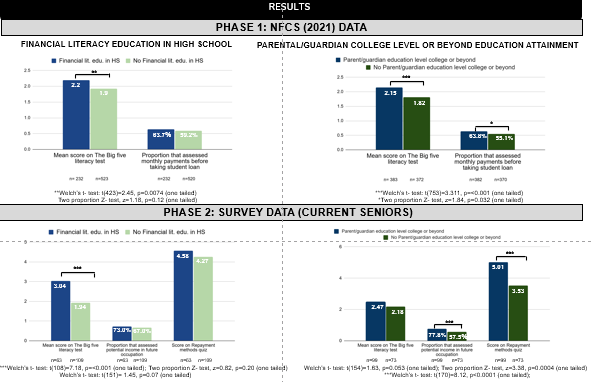

Addendum: I conducted a study and added results here and on the webpage.

Comments